Chapter 48 — Policies to Correct Disequilibrium in the Balance of Payments

Cambridge International AS & A Level Economics (9708) · Unit 11.1 · 4th edition coursebook

Learning objectives

- Explain the components of the balance of payments: current account, financial account and capital account.

- Evaluate the effects of fiscal, monetary, supply-side, protectionist and exchange rate policies on the balance of payments.

- Explain the difference between expenditure-switching and expenditure-reducing policies.

Key terms

- net errors and omissions

- A figure included to ensure the balance of payments balances; sometimes called the balancing item.

- expenditure switching policy

- Policy tools designed to encourage people to switch from buying foreign-produced products to buying domestically produced products.

- expenditure reducing policy

- Policy tools designed to reduce imports and increase exports by reducing demand.

48.1The components of the balance of payments

The balance of payments records every economic transaction between residents of a country and the rest of the world over a given period. The account is split into three main parts — the current account, the capital account and the financial account — together with a balancing entry called net errors and omissions. For some economies the financial account is the largest of these components, while in essay questions the current account and the financial account are the two parts that usually deserve most attention.

Key concept link — Equilibrium and disequilibrium

While the combined accounts of the balance of payments should come to zero, the individual accounts are not usually in balance.

The financial account

The financial account records movements of funds into and out of the country and has four parts. Direct investment covers the building of a new plant in another country or the takeover of an existing firm there. When the country's own firms do this abroad it appears as a debit; when foreign firms do it inside the country it appears as a credit. Portfolio investment records the purchase and sale of government bonds and of shares that do not give the buyer legal control of a firm. Other investments capture shorter-term financial flows including bank deposits, bank loans and inter-government loans. Reserve assets are the central bank's holdings of gold, foreign exchange reserves, Special Drawing Rights (a form of international money created by the International Monetary Fund) and the country's reserve position in the IMF. Reserves are held to settle international debts and to influence the exchange rate; additions to reserves are debit items, reductions are credits, because selling foreign currency brings domestic currency back into the country.

A common confusion is between items that belong in the financial account and items that belong in the primary income part of the current account. The rule is that the investment itself goes in the financial account, while the income the investment generates (profit, interest, dividends) goes in primary income on the current account.

Key concept link — Progress and development

An inflow of direct and portfolio investment can have an impact on progress and development. There are debates about whether multinational companies promote or harm development.

A financial account deficit

A financial account deficit is not automatically a problem. It may simply mean that the country's residents are investing more abroad than foreigners are investing here, which will generate inflows of profit, interest and dividends in later years. A deficit may also be short-term, caused by hot money leaving in search of higher interest rates abroad or in the expectation that other currencies will rise in value. It becomes more worrying when it reflects a sustained loss of confidence in the country's economic prospects. If residents begin moving money to foreign banks and firms shift production overseas — a capital flight — tax revenue falls, potential employment and growth are lost, and the currency is likely to depreciate.

A financial account surplus

A surplus arises when more direct and portfolio investment and loans enter the country than leave it, often because foreign investors view the country's prospects favourably. It can finance a current account deficit, create domestic employment and lift the rate of economic growth. In the long run, however, the inflow generates outflows of profit, interest and dividends, which can push the primary income balance into deficit unless the country also builds up its own investments abroad.

The capital account

For most countries the capital account is small. It records non-produced, non-financial transactions such as government debt forgiveness, money brought into or taken out of the country by migrants, and the sale and purchase of copyrights, patents, trademarks and mineral rights.

Net errors and omissions

The balance of payments as a whole must always balance, because every credit item has a matching debit item somewhere. If a country sells exports (a credit), the foreign buyer needs the country's currency, which they obtain by, for example, borrowing from the country's banks (a debit). In principle, a current account deficit must therefore be offset by an equal surplus on the combined capital and financial accounts. In practice, with millions of transactions, mistakes and omissions occur, and the net errors and omissions figure is added to make the sum equal zero. If the recorded transactions sum to minus $2000 million, an entry of plus $2000 million is added, implying that $2000 million more came in than was captured. As record-keeping improves, the size of this balancing item usually shrinks. By the same logic, world current account deficits should match world current account surpluses, but in practice they do not, again because of measurement gaps.

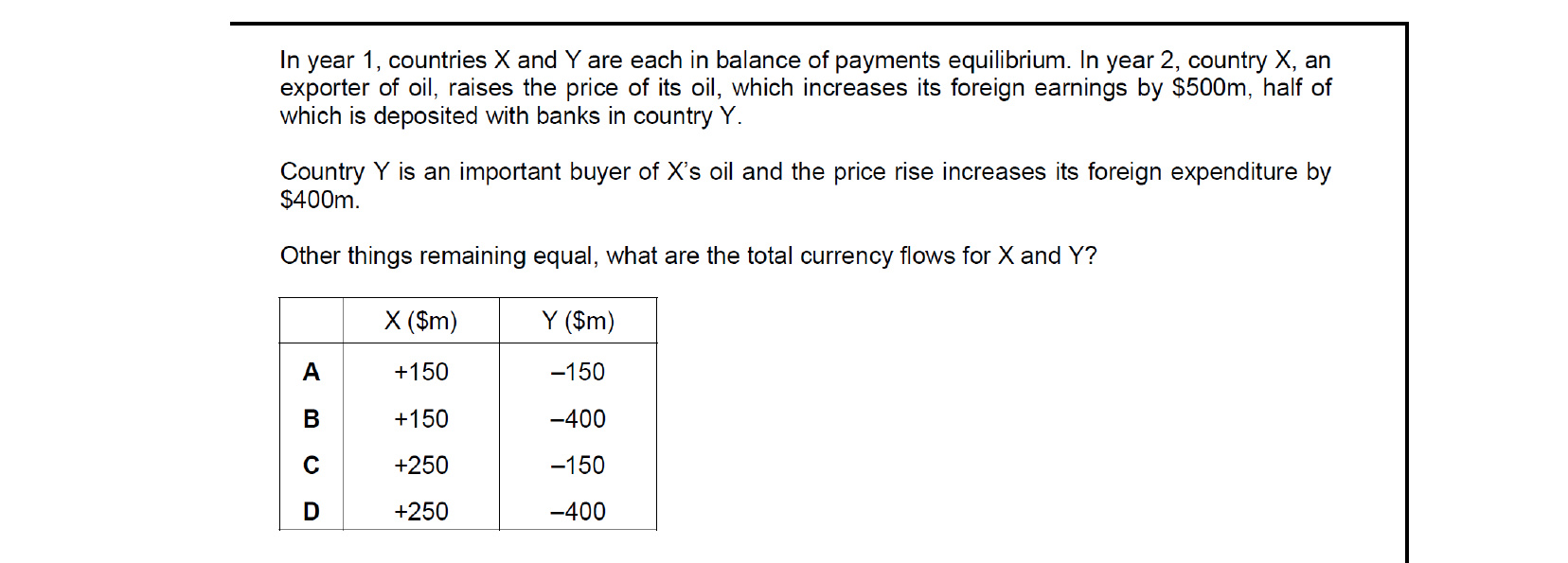

Country X earns $500m extra, of which $250m is spent abroad (deposited in Y's banks) — a financial-account outflow — and $250m stays as a current-account inflow, leaving a net inflow of +$250m. Country Y pays $400m more for oil, but receives $250m back as foreign deposits, giving a net outflow of −$150m. Hence the totals are +$250m for X and −$150m for Y.

48.2Effect of fiscal, monetary, supply-side, protectionist and exchange rate policies on the balance of payments

A government and its central bank have a toolkit of policies to influence the balance of payments. Contractionary fiscal policy (higher taxes, lower government spending) and contractionary monetary policy (higher interest rates, tighter credit) reduce demand inside the economy, which lowers spending on imports and can push firms to send more output to the export market. Supply-side policy works on productive capacity and international competitiveness by raising the quantity and quality of factors of production. Protectionist policy — tariffs, quotas, subsidies, embargoes — tries to replace spending on imports with spending on domestic substitutes. Exchange rate policy changes the relative price of exports and imports.

Which policy can do which job

Fiscal, monetary and exchange rate policies are flexible enough to be aimed at either a deficit or a surplus on the current account. Supply-side policy, by contrast, is essentially a tool for reducing a deficit, because it works by improving competitiveness rather than by curbing demand. Protectionist policy is also most likely to be used to deal with a deficit.

An exchange rate change may only have a short-term effect on the current account. An exception is when a government stops defending a rate that is set above or below its market value. If a central bank has held the exchange rate above the equilibrium level, export prices have been too high and import prices too low, and a current account deficit may have built up; allowing the rate to fall to its market value can then reduce the deficit.

Unintended consequences

A policy aimed at one macroeconomic objective can produce a side-effect on the balance of payments. A cut in income tax intended to reduce unemployment, for example, raises household spending, and some of that spending leaks into imports — widening a current account deficit. Students writing essays should consider both the internal and the external effects of any policy.

Aiming for a financial account surplus

A government that wants to accelerate development or finance a current account deficit may target a surplus on the financial account. Attracting multinational companies raises employment and income growth; selling shares in domestic firms to foreigners gives firms funds to expand; borrowing from abroad can cover the cost of imported raw materials and capital goods that, over time, may strengthen the export sector and reduce the current account deficit. Foreign investors are attracted by macroeconomic stability, so the natural lead policy is supply-side policy. Improvements in education, training, infrastructure and technology raise the quantity and quality of resources and make the economy a more attractive destination. Trade union reform can also help if it reduces industrial action and reassures multinational investors, while privatisation may open new sectors to foreign direct investment. These supply-side measures can take time to work and the outcomes are not guaranteed.

Switching to domestic products

To encourage households and firms to switch from imports to domestic substitutes, a government may impose or raise a tariff on imports. This works best where domestically produced substitutes of acceptable quality exist; where they do not, the tariff simply raises the price consumers pay for imports.

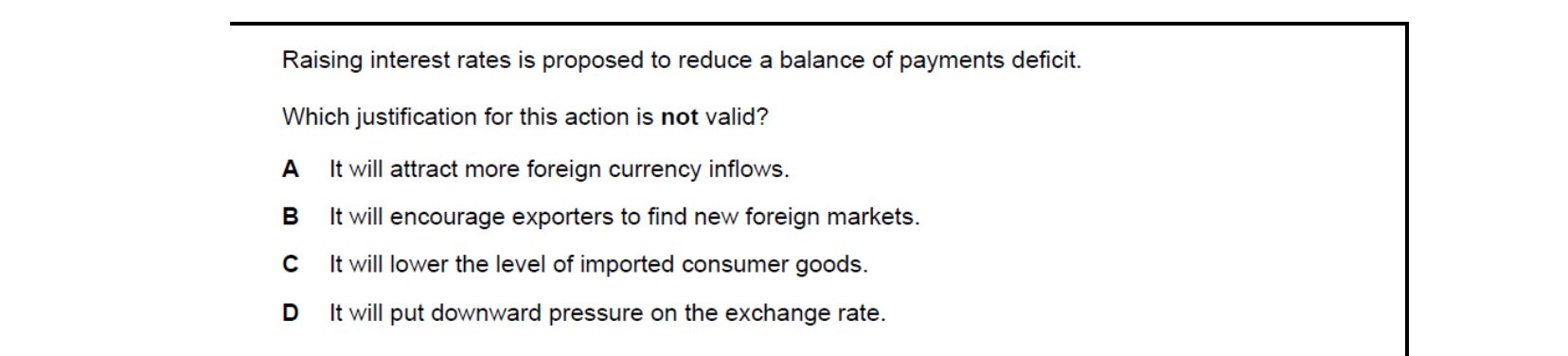

A higher interest rate attracts foreign capital (A), reduces consumer spending and so cuts imports (C), and is intended to support — not weaken — the currency (D would be the opposite of what happens). What it does not do is motivate exporters to seek new foreign markets; if anything, a stronger currency that follows the rate rise makes exports dearer abroad. So justification B is invalid.

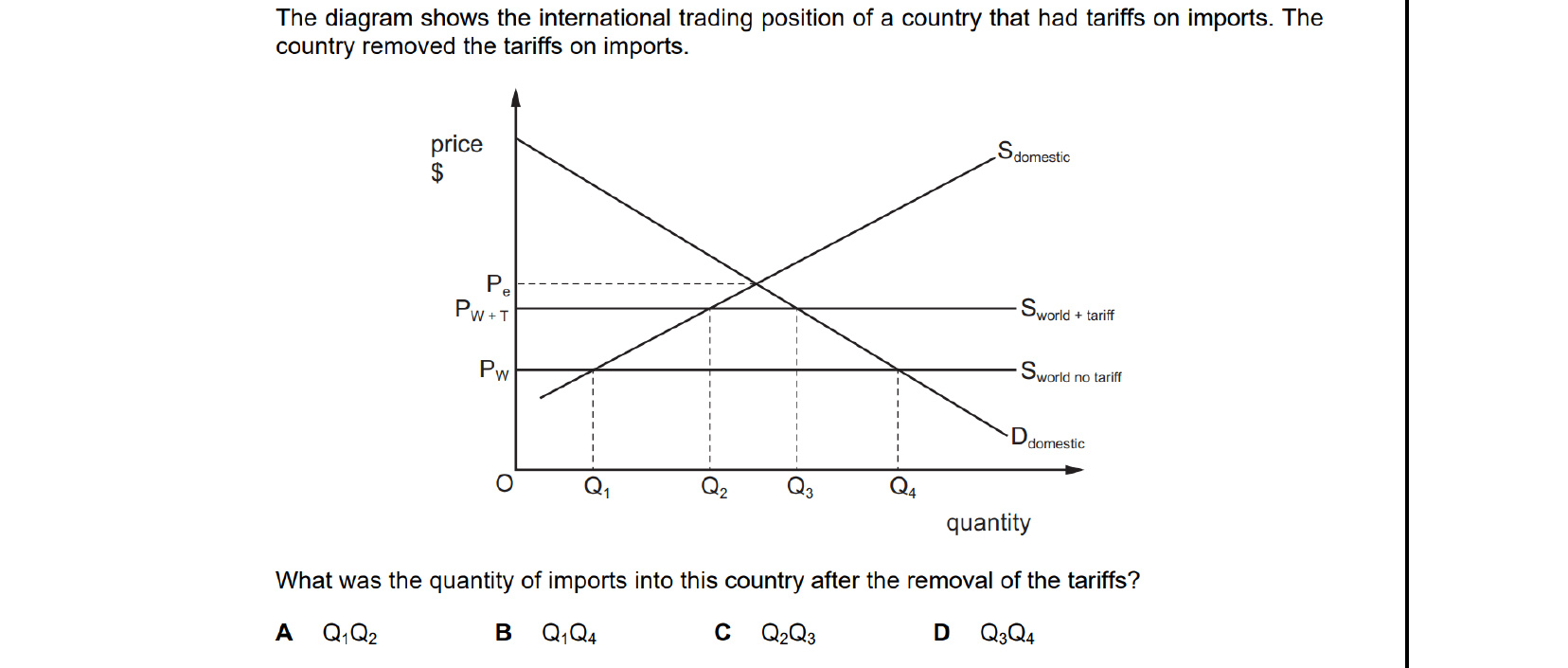

Without the tariff, the world supply curve sits at Pw and the domestic price falls from Pw+t to Pw. At the lower price, domestic supply shrinks to Q1 while total demand expands to Q4. Imports fill the gap between domestic supply (Q1) and total demand (Q4), so the post-removal import quantity is Q1Q4.

48.3Expenditure-switching and expenditure-reducing policies

The policy tools above can be grouped into two broad approaches to correcting an imbalance in the balance of payments: expenditure switching policy and expenditure reducing policy. The test of which group a tool belongs to is simple — ask whether it changes the composition of spending or the total level of spending in the economy.

Expenditure-switching policy

An expenditure-switching policy is any government action that persuades buyers — at home and abroad — to spend more on the country's products and less on the products of other countries. It is not designed to cut total spending; it redirects existing spending towards domestic goods and services. The intended outcome is lower import expenditure and higher export earnings.

The policies most commonly used in this role are supply-side, protectionist and exchange rate tools. Higher infrastructure spending can lower the cost and price of domestic products. An import tariff makes imports more expensive relative to domestic substitutes. A central bank instructed to lower the exchange rate cuts export prices in foreign currency and raises the domestic-currency price of imports.

Key concept link — The role of government and issues of equality and equity

Expenditure-switching policy tools may increase inequality if they increase unemployment.

Expenditure-reducing policy

An expenditure-reducing policy is any government action designed to lower the total level of spending in the economy. It has two channels of effect on the balance of payments. First, lower spending overall means fewer imports are purchased. Second, domestic producers facing a smaller home market may push harder to sell abroad, lifting exports. Together, imports fall and exports rise.

Fiscal and monetary policy are the natural expenditure-reducing tools. The government can raise taxes and cut its own spending. The central bank can reduce the money supply and raise the rate of interest to choke off spending across the economy.

End-of-chapter practice

Past-paper questions from CIE 9708. Pick A, B, C or D. Answers are saved on this device — press Download report (PDF) at the top to save them.

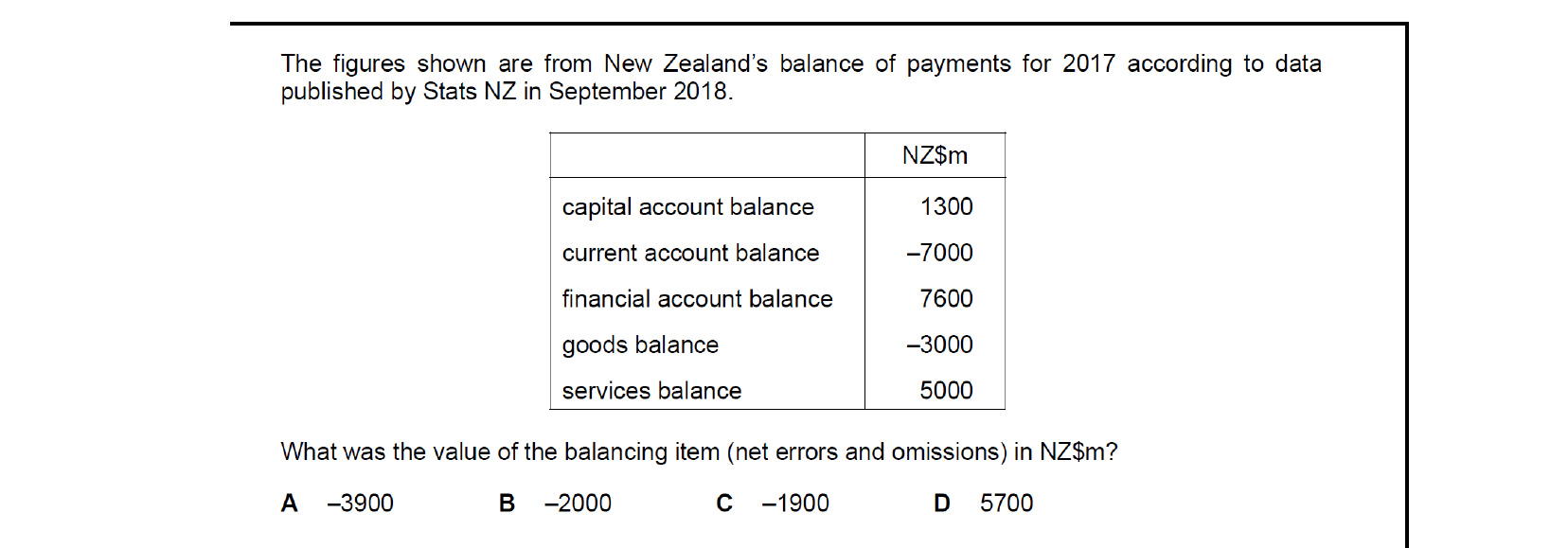

The balance of payments must sum to zero. Adding the recorded balances: capital +1300, current −7000, financial +7600 gives +1900. The balancing item (errors and omissions) must offset this, so it is −1900 NZ$m.

The financial account records cross-border ownership of financial and productive assets. An Indian firm supplying investment to build a new factory in Europe is direct investment abroad — a classic financial-account entry. Buying insurance and employing workers are current-account items (services and income); receiving profits from existing foreign factories is also current account (investment income).

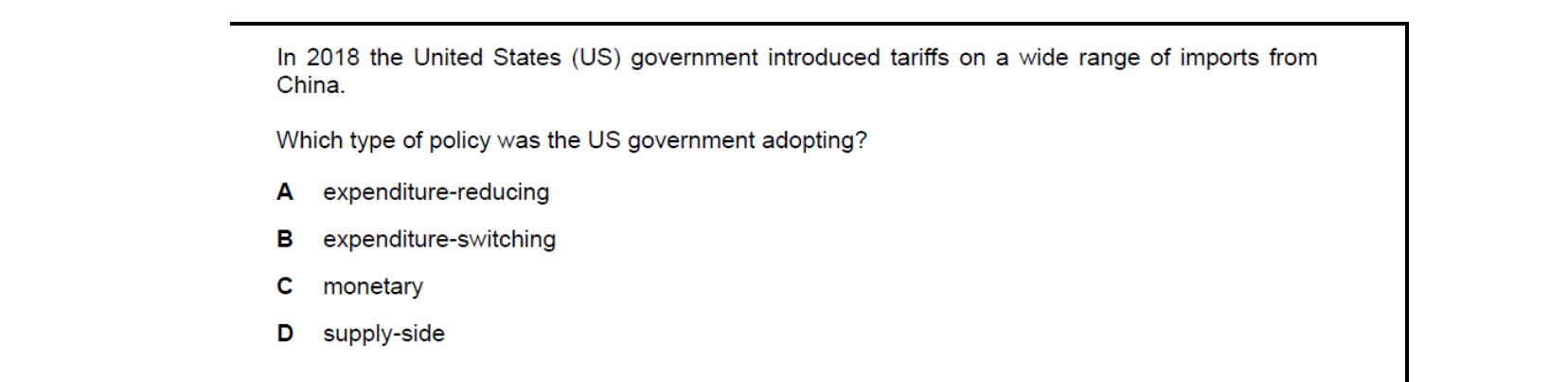

Tariffs make foreign goods dearer relative to domestic substitutes, encouraging buyers to switch their spending from imports to home-produced goods. Total spending is not reduced — only redirected. This is the textbook definition of an expenditure-switching policy. It is not expenditure-reducing (no overall demand cut), nor monetary, nor supply-side.

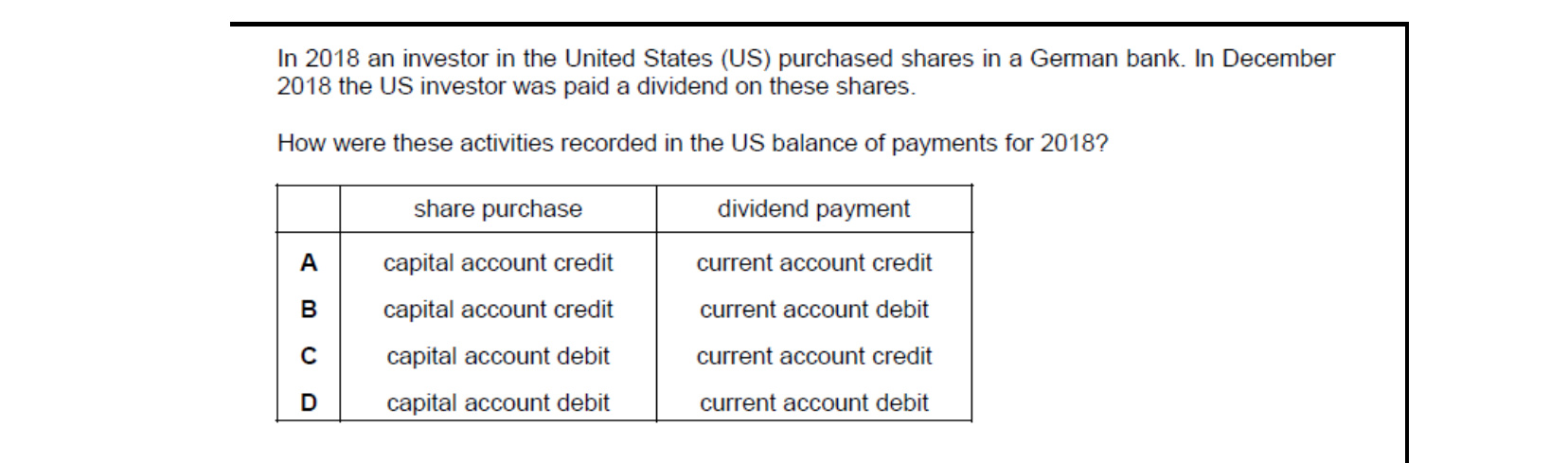

Buying foreign shares is an acquisition of a financial asset abroad — an outflow recorded as a debit in the financial account (the question phrases this as 'capital account' in the older labelling). The dividend received later is investment income, which is a credit on the current account. So the pairing is a capital-account debit and a current-account credit.

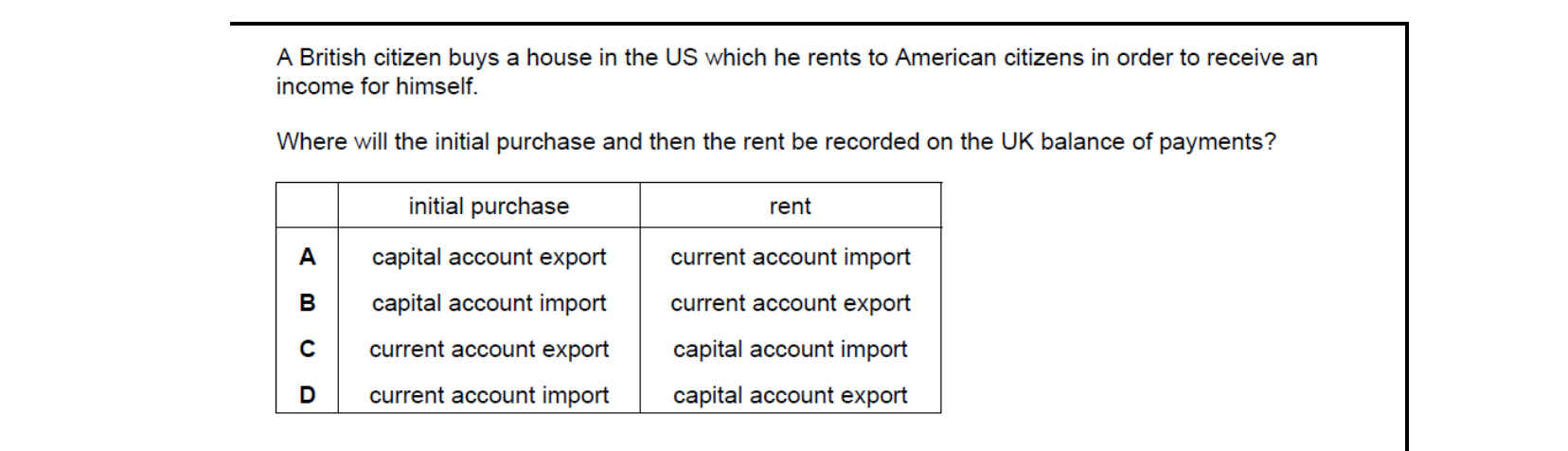

Buying a house abroad is a transfer of capital out of the UK — money leaves the UK to acquire a foreign asset — so it is recorded as a debit (import) on the capital/financial account. The rent received later is income earned from abroad, an inflow that is a credit (export) on the current account. So: capital-account import, current-account export.

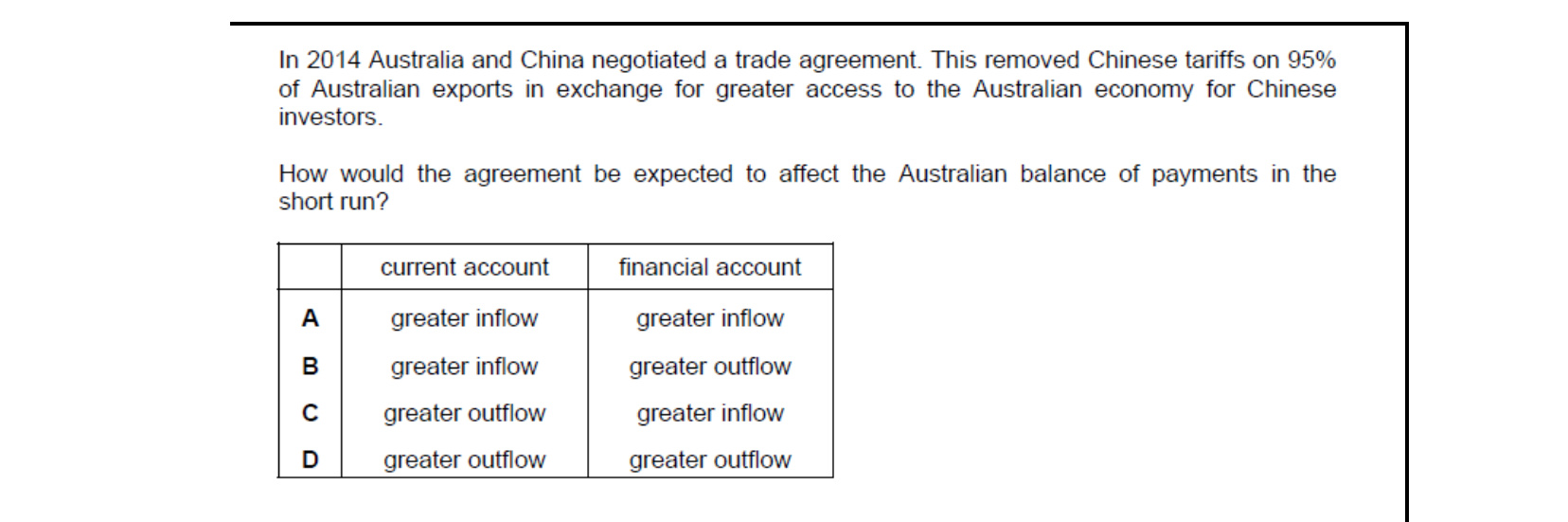

Removing Chinese tariffs raises Australian exports, generating a greater inflow on the current account. Giving Chinese investors better access to the Australian economy brings extra inward FDI, generating a greater inflow on the financial account. So both accounts experience greater inflows.

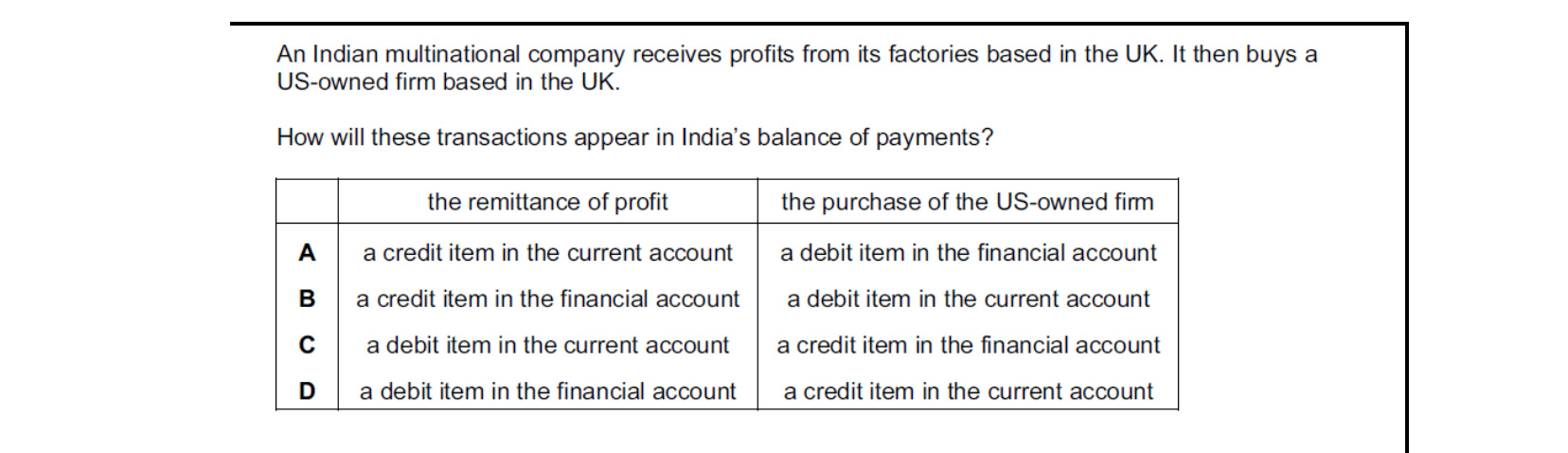

Receiving profits from a UK factory is investment income flowing into India — a credit item on the current account. Buying an existing US-owned firm based in the UK is an acquisition of a foreign asset (FDI outflow) — a debit item on the financial account. So the pairing is current-account credit and financial-account debit.

Attempt the practice questions above to build your score.

Self-evaluation checklist

After studying this chapter, you should be able to:

- Describe the components of the balance of payments: current account (see Section 48.1), financial account and capital account, net errors and omissions.

- Evaluate the effects of fiscal, monetary, supply-side, protectionist and exchange rate policies that governments and central banks may use to influence the components of the balance of payments.

- Explain the difference between expenditure-switching policy tools and expenditure-reducing policy tools that governments may use to correct an imbalance in the balance of payments.

Want more practice? Drill this chapter's past-paper MCQs (61 questions) →